Ben van den Tol, Director, Client Solutions, CBRE Investment Management

The UK commercial real estate market has endured a challenging couple of years, with higher interest rates and economic uncertainty weighing on investment activity. However, signs of recovery and opportunities are emerging, easing inflation and interest rate cuts are helping to stabilise the market and support the recovery. Beyond the broader economic context, the UK property market is undergoing some profound structural challengers as motivated sellers seek exits. These exits are motivated by structural changes within the Pension Fund industry; specifically, DB schemes de-risking and LGPS repositioning, rather than real estate fundamentals. Generally, the assets being sold are of high quality, generate significant cash flow, maintain high occupancy rates, have a diverse tenant mix, and possess attractive residual or alternative use value.

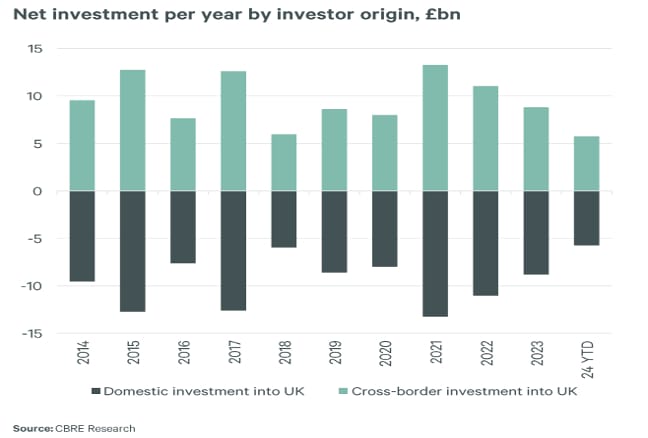

Interestingly, research shows that cross-border investors are steadily replacing domestic investors over the longer term (shown in the chart below). Importantly, this reflects the strong fundamentals of institutional grade UK property on offer and the recapitalisation benefits for new investors with dry powder (80% of buyers are largely US and European institutions). These are good quality assets, being sold for structural issues within the capital stack, rather than distress for the actual asset. 1

As such for DC schemes looking to allocate to private markets, and in turn property, the UK currently offers compelling opportunities to access high quality real estate. Additionally, the current structural dynamics allow for faster deployment times.

Investing in UK property offers more than just financial returns. It aligns closely with the broader objectives of productive finance, contributing positively to both the wider economy and local communities.

Focusing on the residential sector, particularly Affordable Housing, reveals significant economic contributions. According to Lichfields, house building in the UK generates £53 billion in economic output annually and supports nearly 834,000 jobs, with one-third in the construction industry. Additionally, it provides opportunities for 6,000 apprentices, 900 graduates, and 3,300 other trainees each year. The impact of house building extends to local communities, with 20% of the 240,000 new homes built annually being ‘affordable,’ helping families thrive. This development also drives £1.5 billion in infrastructure investment, including £677 million for new and improved educational facilities 2

We remain encouraged by the Government’s reforms to cut planning red tape with the aim of boosting housebuilding to 305,000 new homes per year, with the wider objective of 1.5mn new homes over the next five years.

The 1.7mn people on social housing waitlists, reflecting a 13.6% increase from 2018 through to 2023 is staggering. Notwithstanding, 47% of disposable income spent on rent in London, relative to 34% nationally (outside of London) 3.

The investment proposition for UK property and specifically residential remains profound, not only from a financial impact perspective, but a wider economic and community standpoint. Pension scheme members can benefit from the fundamental attractiveness of the asset class, knowing that their investments positively impact local communities as well as being a significant contributor to the wider UK economy.

Sources:

- CBRE Group research

- Lichfields: The Economic Footprint of Home Building in England and Wales – September 2024

- CBRE Investment Management research