Kurt Walten, Senior Vice President, Investment Affairs & Investor Education, Nareit

The Importance of Underrepresented Asset Classes in Defined Contribution Pension Schemes

For decades, defined benefit (DB) pension schemes have been using real estate successfully within their investment portfolios. This is because most pension schemes consider real estate a fundamental asset class, with unique investment attributes and return drivers, and believe it should be included in all investment portfolios along with stocks, bonds and cash.

The defined contribution (DC) world is rapidly catching up with the DB world in terms of investing in real estate, particularly through the use of listed real estate, including REITs. And for good reason. Past studies conducted by the Center for Retirement Research at Boston College in the U.S., CEM Benchmarking in Canada, and others found that DC pension schemes have underperformed DB schemes and determined that a key driver was the fact that certain asset classes used in DB schemes — such as real estate — are not always made available in DC schemes.

This raises the question, “Are trustees at risk of not meeting their responsibility to beneficiaries because they are not offering diversifying asset classes (like real estate) in their DC schemes that are already used in their DB schemes?” It is a concern that many DC scheme trustees are working hard to address with their investment offerings.

Why Real Estate?

The fact that investment experts consider real estate a fundamental asset class is based on the specific, well-documented attributes of real estate investment, including:

- A distinct economic cycle relative to the cycle for most other equities and bonds due to supply inelasticity, which reduces the correlation of investment returns from real estate with the returns from other assets,

- Competitive, long-term investment returns that potentially provide high and growing income from rents plus moderate capital appreciation over time,

- Potential inflation hedging attributes due in part to the fact many leases are tied to inflation and that real asset values tend to increase in response to rising replacement costs.

Incorporating Real Estate in DC Schemes

For trustees in the UK attempting to determine how best to include real estate in their DC schemes, the U.S. may serve as a helpful model. While DC schemes in the U.S. have been slower than DB schemes to include real estate, their adoption of the asset class in recent years has been rapid. A significant portion of DC schemes have added real estate investment options on a stand-alone basis. However, many more have incorporated this important asset class within their asset allocation offerings, such as their target-date funds (TDFs). In a vast majority of cases, this real estate exposure is gained through an investment in listed real estate, particularly REITs. In fact, a particularly noteworthy development in the asset allocation arena in the U.S. has been the significant increase in both the number of asset allocation products that now include a REIT allocation and the percentage of total assets allocated to REITs within these products.

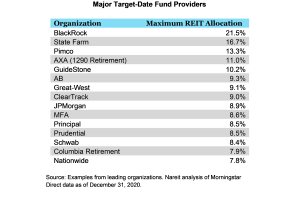

As evidence of this, based on an analysis using Morningstar Direct data, the share of TDFs with REIT exposure increased from 50% in 2003 to nearly 100% in 2019. In addition, 61% of TDFs used in the U.S. now have a dedicated REIT sleeve within their asset allocation. Additional evidence may be found in Exhibit 1, which lists the maximum real estate allocations included in the TDFs of some of the major asset allocation fund providers in the U.S. As of year-end 2020, one allocation topped 20%, and several funds are over 8%.

Exhibit 1

The Growth and Importance of Asset Allocation Products

The growing use of asset allocation products, particularly TDFs, remains the dominant investment-related trend in the U.S. DC market today. In fact, some industry experts believe that a majority of assets in U.S. DC schemes will be invested in target-date products within the next 10 years.

As a result of this trend, DC schemes in the U.S. will continue to gain greater exposure to diversifying asset classes because investing will be done less by scheme members and more by investment professionals – individuals who understand the importance and value of diversification. This trend should have a positive and increasingly substantive impact on DC members gaining exposure to real estate.

Why Listed Real Estate?

Quite simply, listed real estate companies, including REITs, are organisations with a core business of owning stabilised properties, managing them to maximise long-term net total returns, and passing rental income along to investors in the form of corporate dividends. The same set of underlying factors that determine the returns of non-REIT real estate investments—the pace of new construction, occupancy rates, rent growth, investor discount rates, etc.—also determine REIT returns. REITs invest in a broad range of traditional property types including retail centres, apartment buildings, office buildings and industrial warehouses. In addition, the REIT industry has expanded to include infrastructure, data centres, cell towers, timberland and single-family housing. These property types reflect the evolution of the changing U.S. economy; the new economy.

While a limited number of TDFs in the U.S. invest in real estate through “direct” or “private” investment vehicles, most asset allocation products provide real estate exposure exclusively through investments in listed real estate. Usually this is because listed real estate offers low-cost access to real estate, daily market pricing, liquidity and a long-term performance record. From the perspective of a DC scheme sponsor, implementation of listed real estate can be as simple as adding any other fully liquid mutual fund or ETF to their platforms. In short, listed real estate is bought and sold like other stocks, mutual funds and ETFs.

What is an appropriate allocation to listed real estate?

Since 2002, Nareit has been conducting sponsored research with multiple firms including Ibbotson Associates, Morningstar Associates, and Wilshire Funds Management to study the role listed real estate can play within diversified portfolios. These firms have come to similar conclusions, finding that the optimal portfolio allocation to listed real estate may be between 5% and 15%. The appropriate allocation will vary depending on the investor’s goals, risk tolerance and investment horizon. An example of this research is a new Morningstar Associates analysis, which found that the optimal portfolio allocation to REITs ranges between 4% and 13%. See Exhibit 2.

Exhibit 2

The fact that the optimised model portfolios produced by Morningstar and Wilshire feature meaningful REIT allocations is not a surprise given the size of the commercial real estate market. Modern portfolio theory emphasises the importance of diversification within a portfolio (maximising returns and reducing volatility) and well-diversified investment portfolios should include meaningful allocations to all assets in the entire market basket, including real estate.

Commercial real estate is the third largest asset (14%) in the U.S. investment market, after U.S. equities (38%) and U.S. bonds (43%). It is important to note that, while REITs only represent an estimated 10%-20% of the real estate asset figure, research by organisations such as CEM Benchmarking have found that Equity REIT returns are highly correlated with other forms of commercial real estate. It is for this reason that REITs are used to gain commercial real estate exposure in a portfolio. REITs and listed real estate securities may also be used to gain meaningful exposure to the global commercial real estate market basket.

Conclusion

While most DB schemes have recognised the fact that — like stocks, bonds, and cash — commercial real estate is a core asset class and should be included in well-diversified portfolios, DC schemes presently lag in their use of real estate, but are catching up rapidly. In determining how best to provide access to real estate, DC schemes in the U.S. may serve as a helpful model to DC schemes in the UK. For a large population of Americans, the single most important tool for advancing retirement income security is now the set of TDFs in which they can invest through their employer’s DC scheme. While TDFs have several perceived advantages over other investment options, one of the most significant is that they make it possible for investors to invest in the real estate asset class through listed real estate, including REITs, at some level approaching the optimal allocation.

In order to ensure plan members are meeting their pension income goals, scheme trustees would benefit from ensuring that a meaningful allocation to real estate — a sizable asset class — is made available through their investment platforms. As a practical matter, the simplest, lowest-cost and fully liquid means of doing this is to make TDFs available to plan members and ensure these funds include an allocation of at least 5%, and up to 15% or more, to listed real estate.