Authors: Jonathan Barry, FSA, CFA, Managing Director, Jeri Savage, Retirement Lead Strategist, Martina Jersakova, CFA, Director – Institutional, UK, Kim Crabtree, Relationship Director

While auto enrollment has been a success in improving pension coverage, an aging population, low savings rates and increasing life expectancy presents the UK with a broad retirement challenge. In our Retirement Insights paper we considered what lessons the UK can learn from other countries at different points in their retirement income journey.

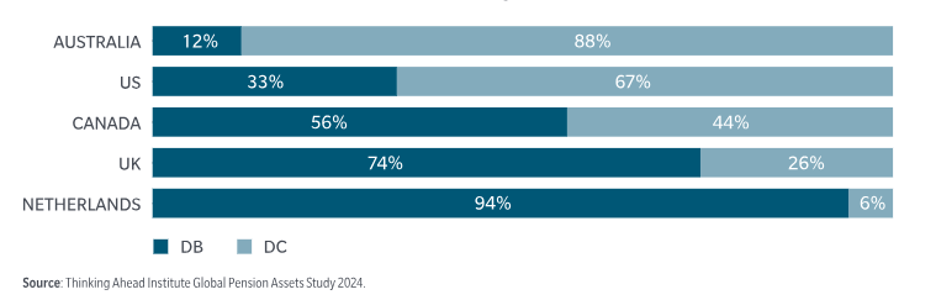

DB Versus DC Assets for the Largest Pension Markets

In this blog we focus on two of the countries that are on opposing ends of the spectrum — Australia, with a mandatory DC system since 1992 and nearly all assets in DC schemes, and the Netherlands, where recent Dutch pension legislation mandates most DB schemes convert to DC by early 2028.

Australia has focused on decumulation and retirement income solutions for the past decade. Since 2022, it is a requirement for superfunds to prepare a retirement income strategy for all members. As a principle-based system, it intends to encourage development of innovative solutions for members. As such, the system compels schemes to formulate and document a principles-based retirement income strategy for their members, focusing trustees on solutions that work for their members rather than reacting to product development. We would encourage UK schemes to document their own retirement income roadmap, detailing their philosophy on retirement income and their key objectives for member outcomes. Only after this is developed, can schemes make informed decisions on products and solutions that fit member needs.

In the Netherlands, schemes are expected to have combined employer/employee contributions above 25%, collective investment programs with age and risk-based asset allocations, and risk sharing features such as smoothing investment returns over time and allowing for variable benefits or limited cost of living increases in case of adverse experiences. While the new system has parallels to the Royal Mail CDC, a key philosophical difference between the Netherlands and the rest of the world is their system is based on better outcomes for all members, rather than individual experience. Convincing members that they can be better off by pooling experience rather than “going it alone” could be a critical component to driving effective retirement income solutions. Also, the significantly higher contribution rates than we currently see in the UK, will undoubtedly drive better outcomes for Dutch savers. While attention is rightly being directed towards retirement income, the UK needs to focus on increasing contribution rates by both members and employers.

While the retirement income challenge is daunting, the UK can benefit from the best practices and learnings of other regions. The master trust and CDC systems also give the UK a structural advantage, offering an opportunity to use scale to drive better outcomes.

The UK can leverage a principles-based approach to help provide members with the solutions they are looking for and, to the extent that products are part of the answer, they should be simple to understand, flexible and portable. Finally, it is important to remember that every member’s circumstances are different, and there is no one-size-fits-all solution that will solve the problem. Thus, providing members with access to high-quality guidance will be a key component of any successful solution.

FOR INSTITUTIONAL AND INVESTMENT PROFESSIONAL USE ONLY

The views expressed are subject to change at any time. These views are for informational purposes only and should not be relied upon as a recommendation to purchase any security or as a solicitation or investment advice from the Advisor. No forecasts can be guaranteed. Unless otherwise indicated, logos and product and service names are trademarks of MFS® and its affiliates and may be registered in certain countries. MFS® does not provide legal, tax, social security or accounting advice. Clients of MFS should obtain their own independent tax and legal advice based on their particular circumstances. No forecasts can be guaranteed.

Note to UK readers: Issued in the UK by MFS International (U.K.) Limited (“MIL UK”), a private limited company registered in England and Wales with the company number 03062718, and authorised and regulated in the conduct of investment business by the UK Financial Conduct Authority. MIL UK, an indirect subsidiary of MFS®, has its registered office at One Carter Lane, London, EC4V 5ER.60932.1