Elaine Alston, Managing Director – UK Institutional Relationship Manager at MFS, MFS

Tackling the gender pensions gap

Women face unique issues as they save for retirement, currently resulting in a 40% lower annual pension income than men[1] which is double the gender pay gap[2].

But what is causing the gap and how can the industry help to tackle it?

In a recently published white paper, MFS evaluated five issues creating the gender pension gap:

– Gender pay gap

– Lack of access to workplace pension schemes

– Career breaks creating disruptions to retirement savings journeys

– Lower confidence in planning for retirement

– Longer life expectancy for women than men

We believe taking some of the following steps would close the disparity and help women secure a better income in retirement:

– Better understanding of what drives the final pot size

Simply saving at the minimum auto-enrolment contribution rate may not bring the desired retirement pot size. Since investment gains play a larger and larger role as the pot size grows, the importance of saving as much as possible as early as possible cannot be underestimated. For DC members in workplace pension schemes, employers can help by matching employee contributions as much as they can.

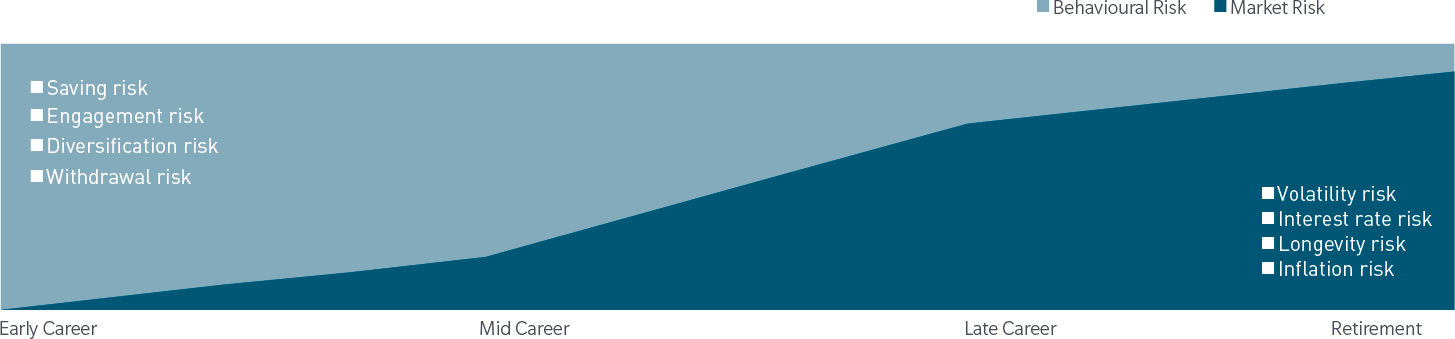

– Increased awareness of how DC member risks evolve

Education on how DC member risks evolve over time would allow women to focus on the most relevant risks given their career stage. As shown below, behavioural risks dominate during the early stages of a career and are eventually replaced by market risks as retirement age approaches. For example, it could be made clear that not saving enough is a key risk early on while the risk from investment losses increases significantly closer to retirement.

Total risk experienced by a DC member

For illustrative purposes only.

– Greater consideration of the impact of excess returns (alpha)

While it may be difficult to avoid career breaks during the retirement savings journey, a renewed focus on building alpha-oriented accumulation strategies could reduce the impact of missing pension contributions during these times. The compounding effect of investment returns means that, over the long term, even incremental alpha can have a significant real-life impact for DC members. MFS analysis showed that an additional 1% of alpha per annum during would result in an ending balance for a double disruption (early and late career breaks) close to the base case scenario of no disruptions and no alpha.

– Increase auto-enrolment participation rates

Additionally, from a policy perspective, we believe there is room to improve the effectiveness of auto-enrolment. In particular, more part-time working women could be auto-enrolled if the earnings threshold was lowered or removed. Thankfully, this is already under consideration by the government.

It is heartening to see government and employer attempts to tackle the gender pay gap in recent years. Looking ahead, we must apply the same focus and combined effort to reduce the gender pension gap.

You can find the full analysis in MFS’ white paper

Elaine Alston joined MFS in 2007 as a Relationship Manager, responsible for the overall client experience. She is a member of the UK Institutional Business Leadership team with specific responsibility for DC.

For institutional and investment professional use only. Issued in the United Kingdom by MFS International (U.K.) Limited (“MIL UK”), a private limited company registered in England and Wales with the company number 03062718, and authorised and regulated in the conduct of investment business by the UK Financial Conduct Authority. MIL UK, an indirect subsidiary of MFS®, has its registered office at One Carter Lane, London, EC4V 5ER and provides products and investment services to institutional investors globally.

[1] Prospect Union, “Tackling the gender pension gap”, November 2018

[2] Prospect Union report based on 39.5% gender pension gap in 2016-17 and gender pay gap of 18.4% in 2017