Elena Zhmurova, DC Strategist, Invesco

Multi asset strategies – particularly diversified growth funds (DGFs) – have found a broad appeal within defined contribution (DC) portfolios due to their potential to provide an attractive combination of growth, diversification, and lower volatility within a single investment vehicle.

However, the differences in the investment approach across the various DGF styles must be fully understood when considering an allocation within a DC lifecycle strategy.

In this article we look more closely at the use of multi asset strategies and consider the benefits of an absolute return multi asset strategy in a DC portfolio, such as:

- Positive absolute returns in all market conditions over a specified time period.

- Preserve the absolute value of savings and protect them from both equity and interest rate related market risks particularly towards the end of the lifecycle.

- Serve as a core allocation within a default path targeted towards an income drawdown, while also providing flexibility for DC members who want to remain invested in growth strategies for longer (or those who are undecided on how to use their pension savings).

- Serve as a core component within a self-select lifestyle strategy for DC members with lower tolerance for risk.

ALL DGFS REDUCE VOLATILITY BUT HOW MUCH?

A DC scheme’s investment objectives start with growth and become increasingly complex towards the end of the glidepath. At this stage, trustees face several choices: when to start de-risking, deciding the most appropriate de-risking default and level of investment risk. Compared to defined benefit (DB) plans, most UK DC schemes have a limited governance budget to be able to implement and monitor complex diversification and de-risking strategies in-house and DGFs became an allocation of choice in the UK as a one-stop solution. According to the Pensions and Lifetime Savings Association (PLSA)[i], DGFs are now part of virtually all lifestyle structures for larger DC schemes.

Broadly speaking, DGFs can be categorized into passive, dynamic, and absolute return strategies. Passive and dynamic DGFs are typically implemented through a variety of traditional and alternative asset classes, while absolute return strategies can include relative value ideas and hedging instruments to generate returns less dependent on the direction of the market.

Those DGFs only using an asset allocation approach may still derive most their returns from macro-related factors such as equity beta and interest rates. For example, a PLSA report[ii] found across 27 DGFs direct equity allocation can range from about 20% to 70%. In the chart below we show the distribution of DGFs correlations to equity and bond markets.

3Ys Time Period

We would argue that an actively managed multi asset strategy targeting absolute returns could be increasingly beneficial towards the later stages of a DC lifecycle, especially if it targets low correlation with broad market returns and a higher potential for capital preservation.

CAPITAL PRESERVATION OR GROWTH IN PRE-RETIREMENT– WHY NOT BOTH?

Since the introduction of pension freedoms in 2015, a pension pot no longer needs to be converted into annuities and many DC plans offer an alternative pre-retirement investment choice allowing members to remain invested in diversified growth strategies. Thus, the combination of capital preservation and the potential of an investment strategy to generate growth is particularly valuable for someone in the final stages of accumulation.

The advantages of remaining in low volatility absolute return multi-asset strategies compared to cash or annuities are multiple. They provide a potential for further upside, help to stave off inflation, and give an individual more flexibility and time to decide how to use their pension pot during retirement. For those retirees who hesitate to make retirement decisions or continue to keep their pot in the workplace DC plan for other reasons, remaining invested in an absolute return multi-asset strategy allows to extend the accumulation stage so that the additional growth element can help protect the individual from the possibility of outliving their assets in retirement.

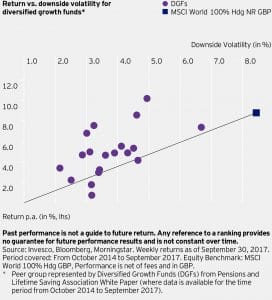

Subsequently, when considering a multi-asset fund for the pre and post-retirement stage the downside volatility and Sortino ratio of a multi asset fund would be a better metric than volatility alone. Since the Sortino ratio measures the fund’s risk/return profile based on its downside volatility, the higher the ratio, the higher the efficiency of the strategy in generating upside per unit of downside risk. As shown in chart below there is wide dispersion in downside volatility across DGFs although the majority has the same target of 1/2 to 1/3 of equities’ volatility. Those DGFs above the line indicate funds with a superior risk/return profile using Sortino ratio than any combination of cash and global equities.

DGFs Returns vs. Downside Volatility

To summarize, absolute return multi-asset funds can play a meaningful role in a DC plan providing genuine diversification and capital preservation benefits especially closer to retirement and beyond. However, the ability of such funds to deliver on the aforementioned benefits is highly dependent on the portfolio manager’s skills, dedicated resources and risk management process. DC plan managers and trustees should be prepared to invest time into thorough research and understanding of such strategy, but the benefits to their DC members can be well worth the effort.

Important information

This document is for Professional Clients and is not for consumer use. Data as at 30th September 2017, unless otherwise stated.

The value of investments and any income will fluctuate (this may partly be the result of exchange rate fluctuations) and investors may not get back the full amount invested. Past performance is not a guide to future returns.

Where individuals or the business have expressed opinions, they are based on current market conditions, they may differ from those of other investment professionals and are subject to change without notice.

As with all investments there are associated risks. Please obtain and review all relevant materials carefully before investing.

Further information on our products is available using the contact details shown.

Issued by Invesco Asset Management Limited, Perpetual Park, Perpetual Park Drive, Henley-on-Thames, Oxfordshire RG9 1HH, UK. Authorised and regulated by the Financial Conduct Authority.

[i] PLSA. Default Fund Design and Governance in DC Pensions report, September 2013.

[ii] PLSA. Diversified Growth Funds, October 2015.