David Blanchett, PHD, CFA, CFP®, Head of Retirement Research, PGIM DC Solutions

Sara Shean, Global Head of Defined Contribution, PGIM Real Estate

As the defined contribution landscape continues to evolve, and particularly as income solutions are prioritized, U.S. Real Estate Debt may be a valuable diversifier to help improve member outcomes. Let’s explore the potential benefits of private real estate debt compared to other asset classes commonly used as diversifying strategies in the fixed income space.

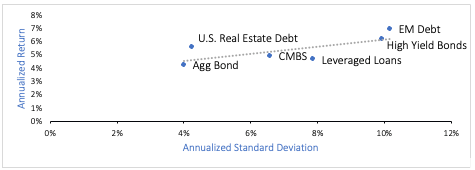

Among the asset classes below, U.S. Real Estate Debt has the highest historical risk-adjusted returns as measured by the Sharpe Ratio. While a few other asset classes had higher returns over the period, they’ve exhibited significantly higher volatility.

Annualized Standard Deviations and Annualized Returns (1Q97 – 4Q22)

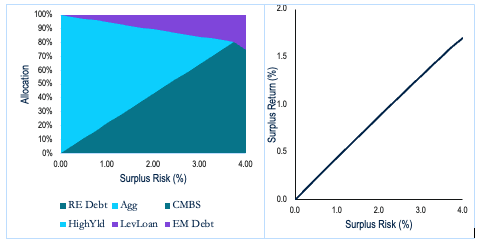

We then wanted to understand how the various asset classes would have potentially improved the efficiency of a fixed income portfolio by running a series of surplus optimizations. We defined the liability for the surplus optimizations as the returns of the Bloomberg US Aggregate Bond Index. Therefore, the results of the optimization provide context as to the optimal weights among the considered asset classes for investors who are interested in moving away from a traditional core bond exposure by introducing, or increasing the potential weights to, other fixed income asset classes.

The charts below provide context on the allocations to the respective asset classes for varying levels of surplus risk, as well as information about how the return impact (i.e., surplus return) varies for each of the efficient portfolios.

Asset Class Allocation vs. Surplus Risk (%) and Surplus Return vs. Surplus Risk (%)

For an investor desiring no surplus risk versus the Bloomberg Aggregate Bond Index, he or she would allocate 100% to US Aggregate Bonds. Moving into the positive surplus risk space, the allocations increase to U.S. Real Estate Debt and Emerging Markets Debt. While allocating away from US Aggregate Bonds into U.S. Real Estate Debt and Emerging Markets Debt introduces surplus risk into the portfolio, it has a notable positive impact on expected (surplus) return, which would have resulted in higher risk-adjusted performance for investors.

Conclusions

Overall, this analysis provides compelling evidence for the historical benefits of including U.S. Real Estate Debt as part of a fixed income portfolio, especially for investors interested in moving into asset classes that have the opportunity to generate higher returns at marginally higher risk levels. Professional management, combined with strong risk-adjusted returns and enhanced yield potential, creates an attractive proposition for consideration within defined contribution schemes.

This report is intended for Institutional and Professional Investors only. All investments involve risk, including the possible loss of capital. The presenters in this report are expressing their views, opinions and recommendations regarding economic conditions, asset classes, securities, issuers and/or financial instruments. The views expressed in this report are for informational or educational purposes only. The information is not intended as investment advice and is not a recommendation about managing or investing assets. In providing these materials, PGIM is not acting as your fiduciary. REF: 009033

For more information, please visit pgimrealestate.com.