In Brief

- Investment returns matter. A lot. Whilst contributions serve as the foundation for future investment gains, it is the accumulation of investment returns over time that ultimately drives Defined Contribution (DC) member outcomes.

- The journey is important. The long-term time horizon should allow DC schemes to harness the considerable power of compounding, but behavioural biases and changing circumstances can often prevent members from taking full advantage of it.

- A low volatility equity strategy may bring advantages that are very well aligned with DC schemes because they can address these issues.

Compounding

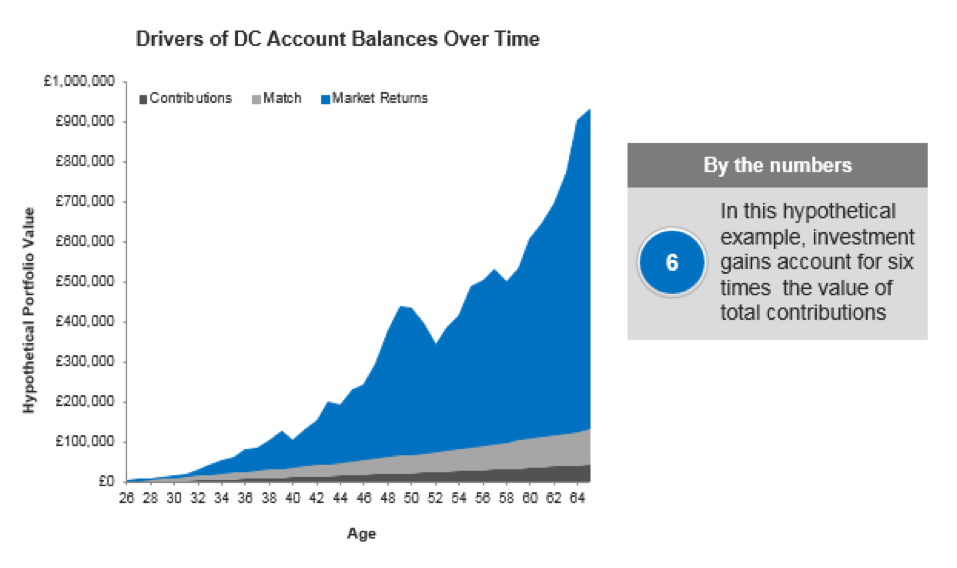

We asked ourselves what really drives member outcomes. The chart below shows that, using very prudent assumptions, the gain from investment returns is worth six times the level of contributions over the lifetime of an average DC member. That is not to say that contribution rates are not important — at the very least they serve as the foundation for future investment gains — but rather that it is easy to underestimate the impact that the compounded growth of investments over time has on retirement wealth. Another key takeaway is that the interaction of member engagement and investment returns is extremely important in DC, and a key differentiator of Defined Benefit schemes.

Assumptions: Hypothetical example assumes a 40-year investment horizon (1976-2015) within the context of the MFS proprietary Member Savings Model. Retirement age assumed to be 65 while beginning contribution age is 26. Beginning member salary of £20,000 (at age 22); 2% annual wage growth over 44 years (1972-2015); the proxy portfolio is a 60/40 blend of MSCI World index (net dividend reinvested) and FTSE over 15 year Gilt index (total return) over the same time period rebalanced monthly. A market index is defined as the aggregate value produced by combining several stocks or other investment vehicles together and expressing their total values against a base value from a specific date. Fees of 100 bps are applied to each year’s returns. A basis point is a unit of measure used to describe the percentage change in the value, rate or fee of a financial instrument. 1 basis point is equivalent to 0.01% (1/100th of a percent); 100 basis points is equivalent to 1.0%. Data source for proxy portfolio performance: Morningstar Direct. Average annual returns applied each year to portfolio ending balance plus contributions with the assumption that contributions are made uniformly over the course of a year; Employer contribution is 6.7% of salary; Employee contribution is 3.4% of salary based on Pensions Policy Institute (PPI) Pension Facts March 2015. This is a hypothetical example shown for illustrative purposes only. An investment cannot be made directly into an index. Past performance is not a reliable indicator for future results. All financial investments involve an element of risk. The value of investments may rise and fall so you may get back less than originally invested.

Suffice it to say that compounding is a powerful tool that should be at the disposal of DC members who are able to think long term and stay invested. However, timing risk, sequencing risk and a bias to action (amongst other biases) can significantly impede DC members’ ability to take full advantage of it, which may compromise the most important driver of their retirement outcome.

When it comes to investing DC pensions’ schemes assets, participants face a dilemma. Investing success is reliant on investment gains, which will be achieved in large part through equity investing, yet the risk of market volatility improperly managed can impair members’ outcomes. The traditional approach to managing this risk in DC schemes has been to increase diversification.

Additional option

Low volatility offrings could offer an additional option. In general, these strategies aim to provide risk management during an equity market downturn while still participating in equity markets when they rise. There are many different approaches investors can choose, ranging from active to passive, from qualitative to quantitative, and from real assets to synthetic and other combinations in between.

Many of these strategies target low volatility stocks, which in theory should not generate a better return. The principles of finance are built on the premise that investors should get more return for taking more risk. Therefore, excluding or avoiding volatile stocks should lead to a commensurate drop in expected returns. While this is a useful starting point for analysis and framework for observation, historic experience suggests that this theoretical risk/return relationship does not always hold true. Much has now been written on the ‘low volatility anomaly’. The aspect that we would draw out is that the action derived from it seems to be to focus almost single-mindedly on targeting low volatility stocks. However, we believe that an approach focused too firmly on this creates other, unwanted, outcomes and that the low volatility anomaly is really about avoiding high-volatility stocks rather than targeting low volatility stocks.

With more money flowing into low volatility strategies, there is natural concern that the anomaly may break down. In reality, whilst flows are significantly higher than they were, this approach still makes up a very small proportion of the equity universe. Stocks held within a low volatility portfolio should look very different from those in a value or growth portfolio, with minimal overlap between the three approaches. The main reason for this is because of the difference in the sector allocations and weighting in a low volatility portfolio versus a cap-weighted index. This means that a low volatility strategy often complements other active investing styles and the anomaly should persist.

How does it fit in today’s arrangements? Assuming we start with an equal split between passive equity and popular diversified growth funds (DGFs), is there room for low volatility strategies as well? Our analysis, using a generic low volatility product and three of the most widely used DGFs in the UK market, shows that including low volatility equities as part of the lineup has been a meaningful additive — it historically improved the expected outcome and reduced the downside and range of possible outcomes.

Important Risk Considerations

Investments in historically lower-volatility equity securities may not produce the intended results if lower-volatility equity securities do not outperform the product’s benchmark, if in general the historical volatility of an equity security is not a good predictor of the future volatility of that equity security, and/or if the specific equity securities held by the products become more volatile than expected. It is expected that the product will generally underperform the equity markets during strong, rising equity markets.

Madeline’s comments, opinions and analyses are for informational purposes only and should not be considered investment advice or a recommendation to invest in any security or to adopt any investment strategy. Comments, opinions and analyses are rendered as of the date given and may change without notice due to market conditions and other factors. This material is not intended as a complete analysis of every material fact regarding any market, industry, investment or strategy.

About MFS Investment Management

Established in 1924, MFS is an active, global asset manager with investment offices in Boston, Hong Kong, London, Mexico City, São Paulo, Singapore, Sydney, Tokyo and Toronto. We employ a uniquely collaborative approach to build better insights for our clients. Our investment approach has three core elements: integrated research, global collaboration and active risk management. As at 28 February 2017, MFS manages US$440.8 billion in assets on behalf of individual and institutional investors worldwide.