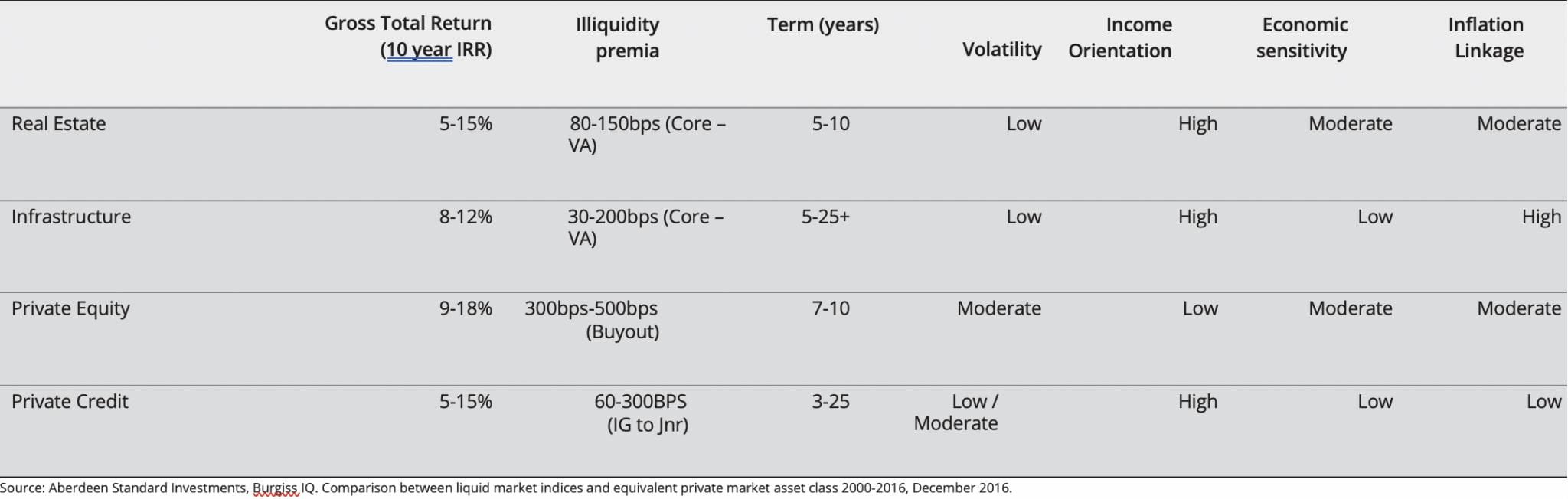

Private markets encompass real estate, infrastructure, private equity and private credit – the land, buildings, systems and services on which our cities and countries depend; investment in business and ventures that are not traded on the stock exchange; and the provision of debt directly to businesses or projects that is not traded on an exchange. Each of these sub asset classes offers different risk and return characteristics.

This has long since been a valuable component of pension investment portfolios. Opportunities in property have widened to include student accommodation, residential housing, logistics, and development assets, which offer the potential for capital appreciation over the long term, combined with cash flows from rents.

Investments in infrastructure have also been embraced by the pension investment community, particularly local government; it is highly valued for its ability to generate predictable, stable and reliable cash flows. Many such investments are natural monopolies and have built-in inflation escalators.

Thanks to the wide range of companies now under private equity ownership, investing in private equity is an increasing component of overall asset allocation among institutional investors. Instead of focusing on quarterly earnings, the average private equity fund will own a company for five to seven years, allowing management teams to drive through operational or strategic improvements in order to maximise revenue and increase profits. Private equity is fundamentally about creating value through the transformation of companies.

Private credit affords investors another means of expanding their opportunity set. While regulatory constraints have curtailed the amount that banks have been willing to lend to businesses and projects, the provision of debt from the private sector has seen substantial growth. Private credit offers a diverse array of strategies and a number of advantages, particularly in a low return environment. Target return, risk and liquidity are among the most important considerations; these strategies offer the potential to achieve different objectives, with differing degrees of liquidity.

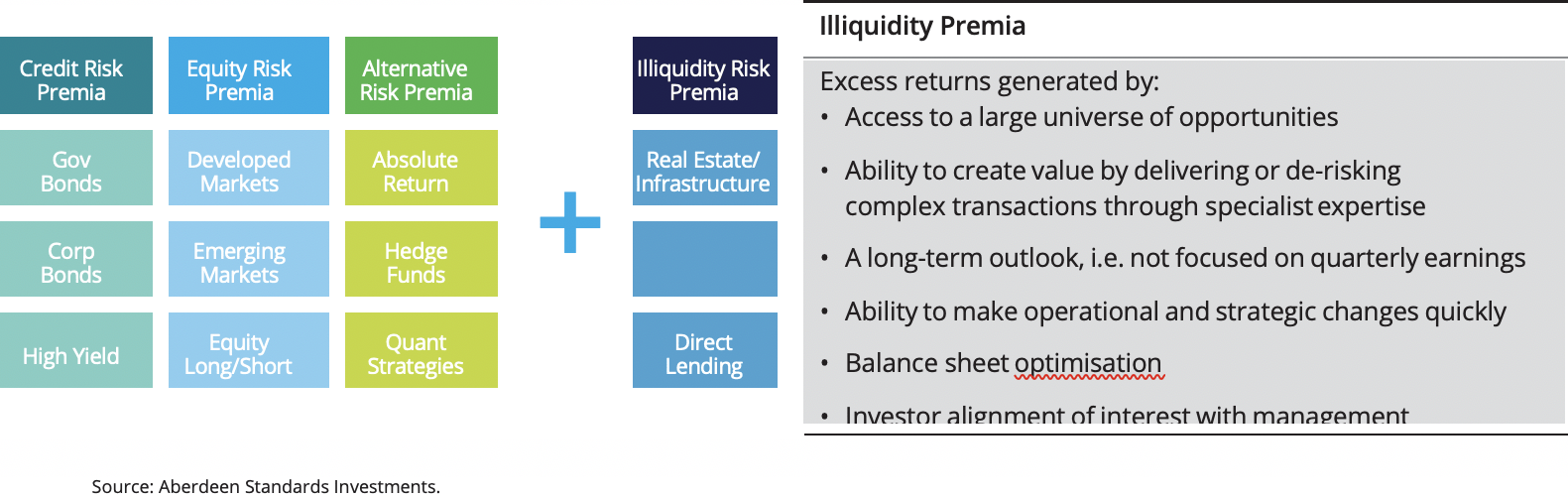

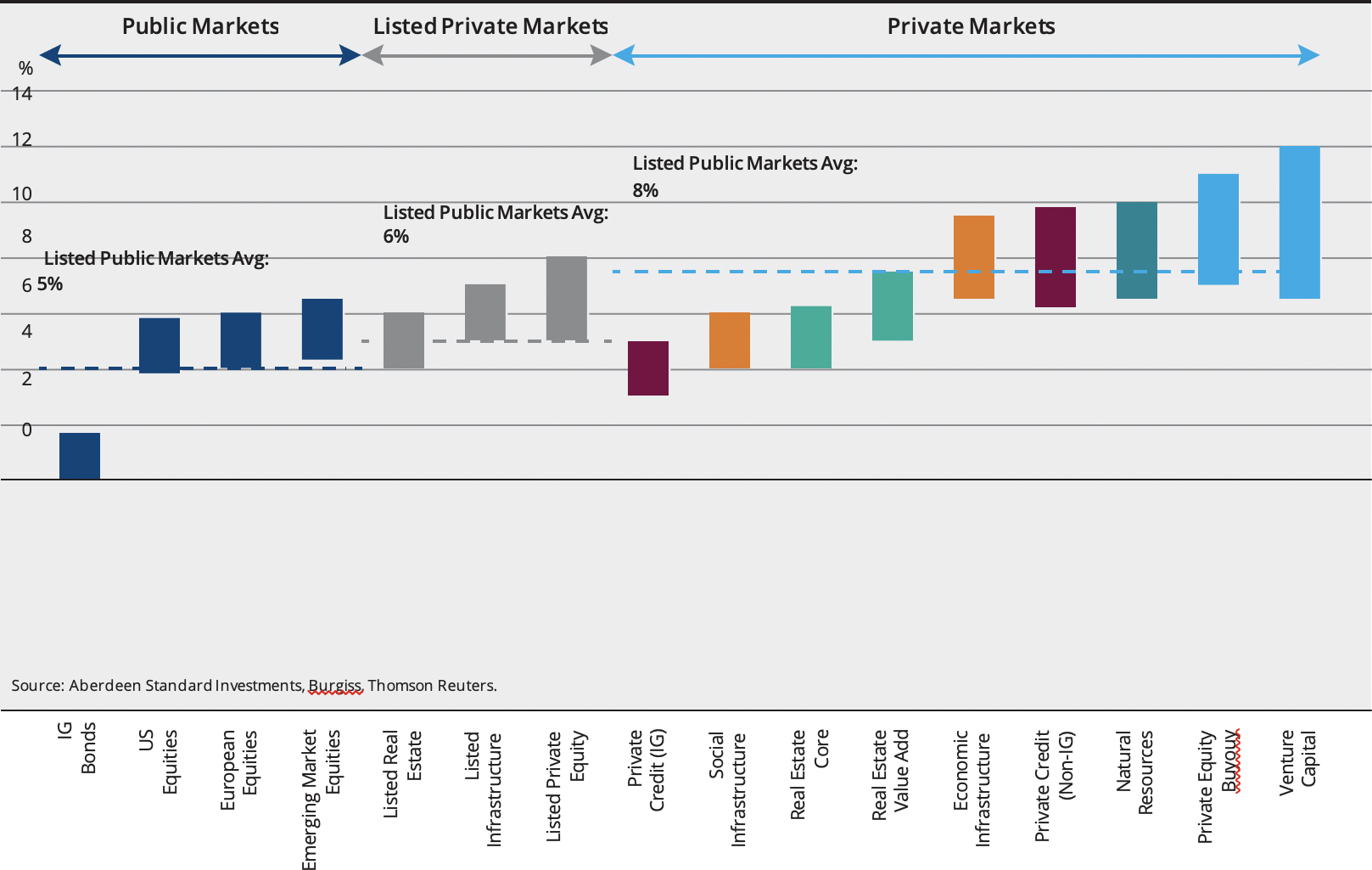

As the chart below illustrates, it is widely accepted that an allocation to private markets can improve the risk-adjusted return potential of a long-term investment portfolio. Here we see the potential to benefit from an illiquidity premium of between 200 and 300 basis points above listed assets, which is a very substantial opportunity.

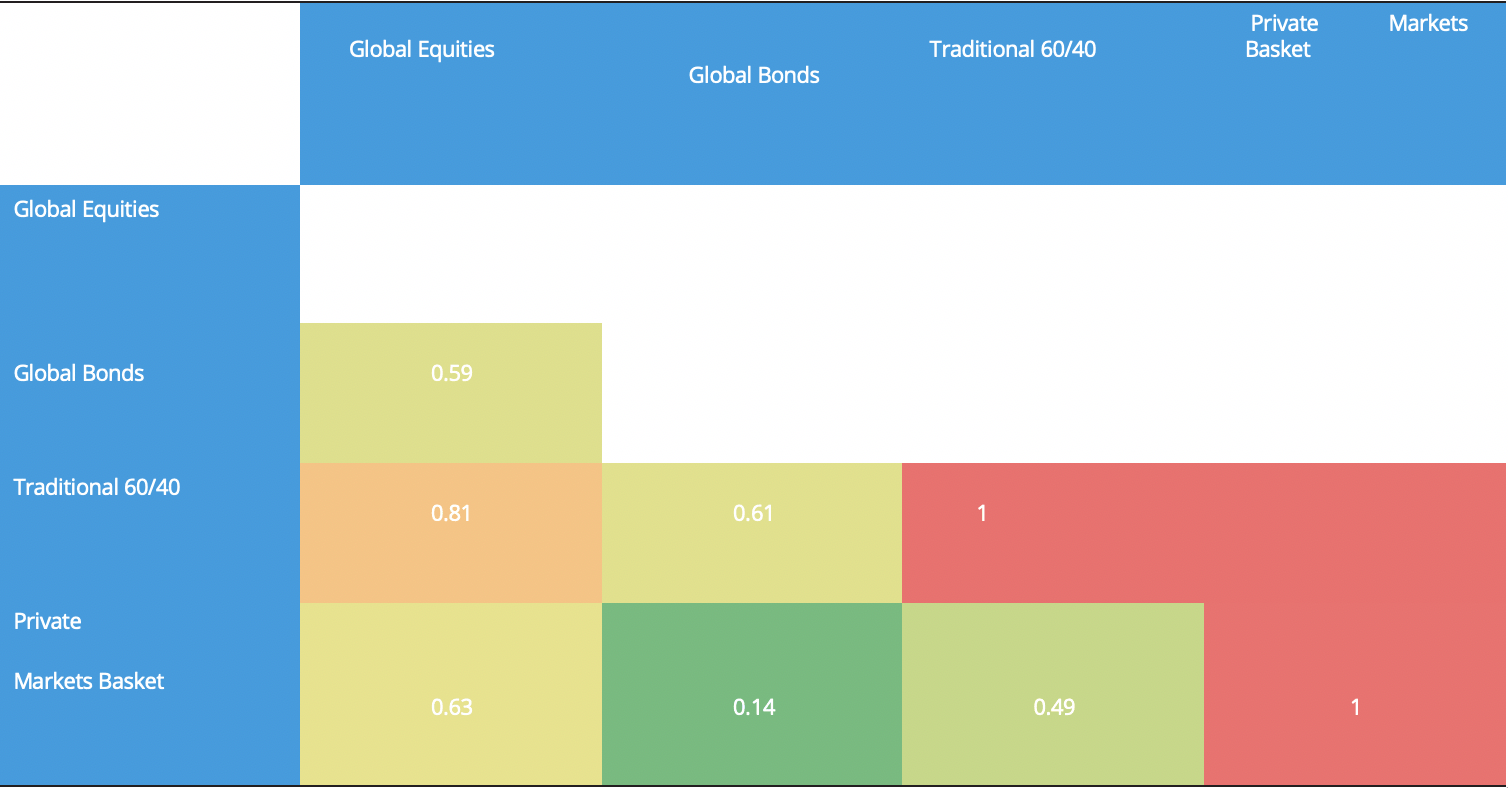

Importantly, private markets offer low correlation of returns to traditional asset classes in public markets, and if this is built into a portfolio, there can be very attractive risk/return benefits.

Many pension professionals will be aware of the exemplary performance of the Harvard and Yale university endowments, which have invested material proportions of their portfolios in private markets for the past two decades, and have consistently achieved very attractive annual returns. These markets need not be off-limits to UK DC schemes. Secondary markets are developing across these sub asset classes and we are working with a number of investors to develop solutions that enable private markets to be part of DC portfolios, leveraging our deep sector experience and expertise in strategic asset allocation, implementation risk, and portfolio risk management.

Important Information

For professional investors only – not for use by retail investors or advisers.

Aberdeen Standard Investments is a brand of the investment businesses of Aberdeen Asset Management and Standard Life Investments.

The above marketing document is strictly for information purposes only and should not be considered as an offer, investment recommendation, or solicitation, to deal in any of the investments or funds mentioned herein and does not constitute investment research as defined under EU Directive 2003/125/EC. Aberdeen Asset Managers Limited (‘Aberdeen’) does not warrant the accuracy, adequacy or completeness of the information and materials contained in this document and expressly disclaims liability for errors or omissions in such information and materials.

Any research or analysis used in the preparation of this document has been procured by Aberdeen for its own use and may have been acted on for its own purpose. The results thus obtained are made available only coincidentally and the information is not guaranteed as to its accuracy. Some of the information in this document may contain projections or other forward looking statements regarding future events or future financial performance of countries, markets or companies.

These statements are only predictions and actual events or results may differ materially. The reader must make their own assessment of the relevance, accuracy and adequacy of the information contained in this document and make such independent investigations, as they may consider necessary or appropriate for the purpose of such assessment. Any opinion or estimate contained in this document is made on a general basis and is not to be relied on by the reader as advice. Neither Aberdeen nor any of its employees, associated group companies or agents have given any consideration to nor have they or any of them made any investigation of the investment objectives, financial situation or particular need of the reader, any specific person or group of persons. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of the reader, any person or group of persons acting on any information, opinion or estimate contained in this document.

Aberdeen reserves the right to make changes and corrections to any information in this document at any time, without notice.

Issued by Aberdeen Asset Managers Limited. Authorised and regulated by the Financial Conduct Authority in the United Kingdom.