Bhavika Patel, Associate Director, BlueBay Asset Management

When the US Federal Reserve lowered interest rates on 30 October, this marked the third reduction in 2019 and got the market talking.

The tri-fold reduction, combined with a commitment by the Federal Reserve to restart bond purchases, looked to many like the return of quantitative easing (QE) measures.

Coordinated QE efforts by central banks around the world boosted the global economy following the fallout of the 2008 financial crisis. The result was a healthy rebound in growth and rising employment rates.

Efforts to unwind these extraordinary monetary loosening, proved short lived and largely unsuccessful. Hence the chatter surrounding three rate cuts in the US as a so-called return to QE.

But we believe things will be different this time around.

Investors have become fearful of being trapped in an ongoing environment of easy financial conditions and persistently low-to-mediocre global growth. Caution will remain until growth green shoots become more firmly established.

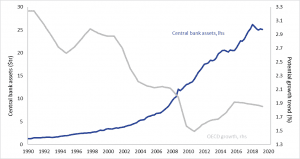

QE anaesthetic for declining growth

Source: OECD, Macrobond. Latest data to Q2 2019.

But while we think a strong rebound isn’t on the cards, mediocre shouldn’t be a dirty word for markets moving into 2020 either.

Easing in financial conditions, combined with signs of improvements surrounding the US/China trade war and a stabilisation in the Chinese economy, should all support a slow-but-steady turn to the positive for global growth.

So, in a world where growth is not ‘hot’ enough to prompt interest rate increases, and not ‘cold’ enough to cause companies to default on their loans, what’s just right for fixed income returns? Or…in porridge terms, what’s looking tasty for 2020?

While traditionally investors have considered equities to be the main beneficiary in growth markets, more so than fixed income, we think the breadth of the fixed income market provides opportunities for investors to benefit from positive returns in the asset class.

One potential opportunity is last year’s underperformers. The 2019 laggards could be the ones to watch as a positive tilt to growth should allow them to play catch-up. We’re predicting that growth-sensitive cyclical assets will outperform, alongside lower-quality credit.

Why lower-rated credit? Because it’s lagged its high-rate counterpart through 2019 but we believe now offers the potential of lower volatility and positive returns in a mediocre growth environment. However, investors cannot be complacent, quality bottom-up credit selection will become even more critical.

Notably, in our view, the banking sector stands out. We think that Bank credit fundamentals have improved dramatically since the financial crisis and bank debt capital offers amongst the most attractive risk-adjusted returns in a low-yield environment.

Elsewhere, we feel emerging markets (EM) also boast opportunities. Despite the hard currency market posting attractive returns in 2019, populism and political risk were striking features on the EM landscape throughout the year for many EM countries.

The challenge for fixed income investors in 2020 could be one of optimal strategy selection, as the opportunity set is broad.

*****************

To learn more about growth in 2020, along with our views on alpha opportunities, see the BlueBay 2020 Global Investment Outlook.

Issued in the United Kingdom (UK) by BlueBay Asset Management LLP (BlueBay), which is authorised and regulated by the UK Financial Conduct Authority (FCA). BlueBay is also registered with the US Securities and Exchange Commission (SEC) and is a member of the National Futures Association (NFA) as authorised by the US Commodity Futures Trading Commission (CFTC). In the United States, it may be issued by BlueBay Asset Management USA LLC which is registered with the SEC and NFA. In Japan by BlueBay Asset Management International Limited which is registered with the Kanto Local Finance Bureau of Ministry of Finance, Japan. In Switzerland by BlueBay Asset Management AG where the Representative and Paying Agent is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich, Switzerland. In Germany, BlueBay is operating under a branch passport pursuant to the Alternative Investment Fund Managers Directive (Directive 2011/61/EU). The registrations and memberships noted should not be interpreted as an endorsement or approval of any of the BlueBay entities identified by the respective licensing or registering authorities. Information herein is believed to be reliable but BlueBay does not warrant its completeness or accuracy. Opinions and estimates constitute our judgment and are subject to change without notice. No part of this document may be reproduced in any manner without the prior written permission of BlueBay. ® Registered trademark of Royal Bank of Canada. RBC Global Asset Management is a trademark of Royal Bank of Canada. Copyright 2019 © BlueBay Asset Management LLP, registered office 77 Grosvenor Street, London W1K 3JR, England, partnership registered in England and Wales number OC370085. The term partner refers to a member of the LLP or a BlueBay employee with equivalent standing. Details of members of the BlueBay Group and further important terms which this message is subject to can be obtained at www.bluebay.com. All rights reserved.