David Whitehair, Director, Institutional DC, Janus Henderson Investors.

Tal Lomnitzer, Senior Portfolio Manager, Janus Henderson Investors.

The energy transition needed to address climate change needs significant investment in new resources capacity. Whilst many pension plans are focused on investing in firms with higher ESG ratings and lower carbon profiles, little thought has been given to the vast quantities of critical enabling raw materials to build the low carbon economy.

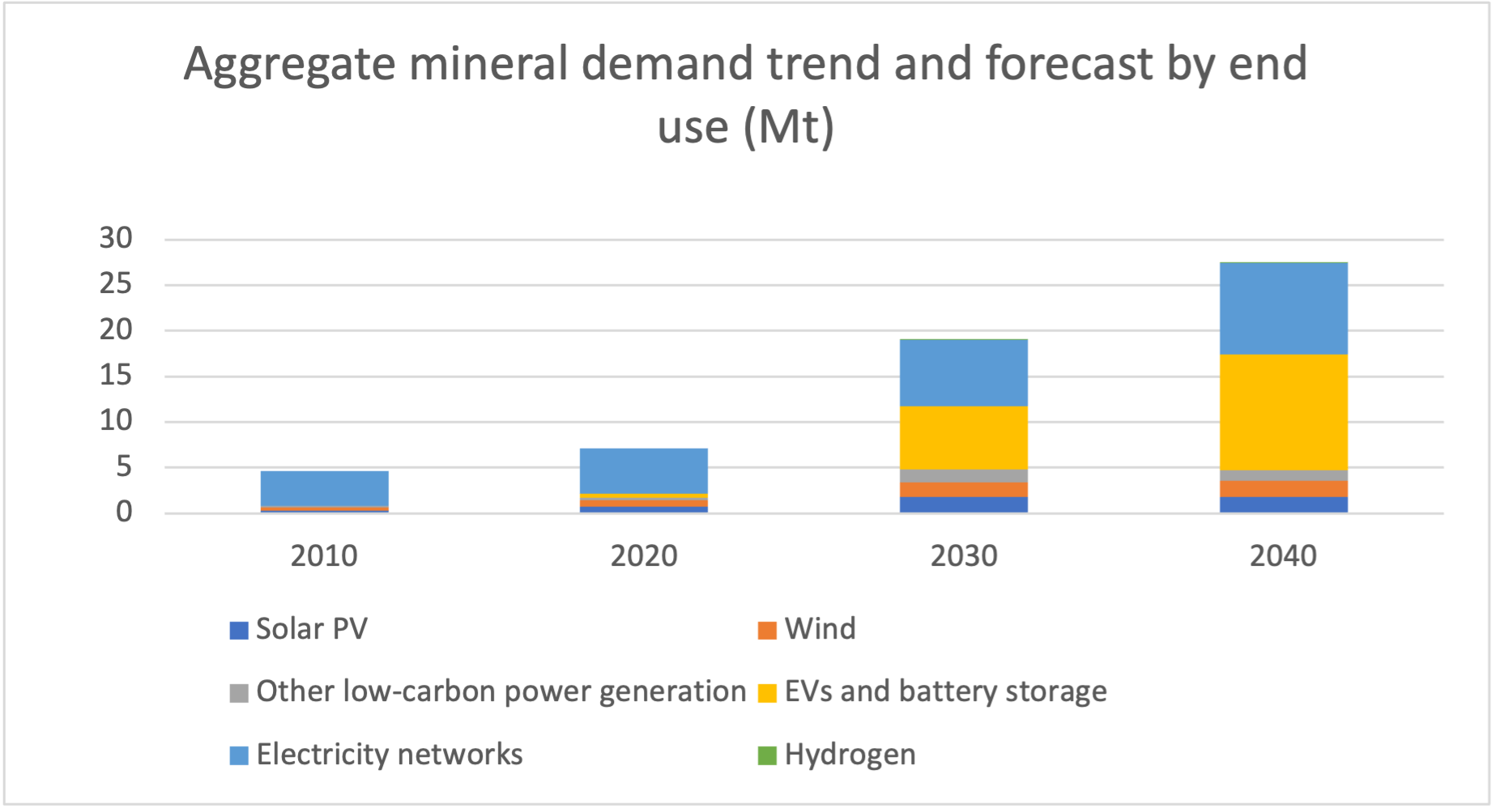

The International Energy Agency (IEA) estimates that countries will have to source over three and half times the total demand from the same end markets in 2020 every year by 2040 to keep track with decarbonisation targets.

Source: IEA as of May 2021. Includes copper, major battery metals (lithium, nickel, cobalt, manganese and graphite), chromium, molybdenum, platinum group metals, zinc, rare earth elements and others, but does not include steel and aluminium. There is no guarantee that past trends will continue, or forecasts will be realised. The views are subject to change without notice.

Despite the obvious pressing need to ramp up supply to meet the demand associated with decarbonisation, global resources firms have yet to materially lift investment in new capacity after a decade of underinvestment that followed the peak spending in 2011 induced by the China-led demand for resources. Most worryingly is that there appears to be no plans to snap out of this period of chronic industry underinvestment with analysts forecasting near-term investments in new capacity across the sector to run in about half the pace seen in the 20 years that preceded the peak of China’s hunger for resources.

The ongoing drive to lower the carbon profile of portfolios means many equity portfolios are now underweight the resources sector and therefore key transition enabling materials at a time when the sector’s capital needs are set to surge. New low carbon and Paris-aligned index approaches have significantly less resources exposure than passive index tracking.

We are advocates of DC Trustees adopting a more holistic approach to decarbonistion by looking at the wider picture of how this can be achieved rather than purely focusing on low-carbon companies and scope 1-3 emissions within portfolios. Currently, the “scope” lens applied to gauge the carbon profile of investments puts resources at a disadvantage in the eyes of carbon conscious investors.

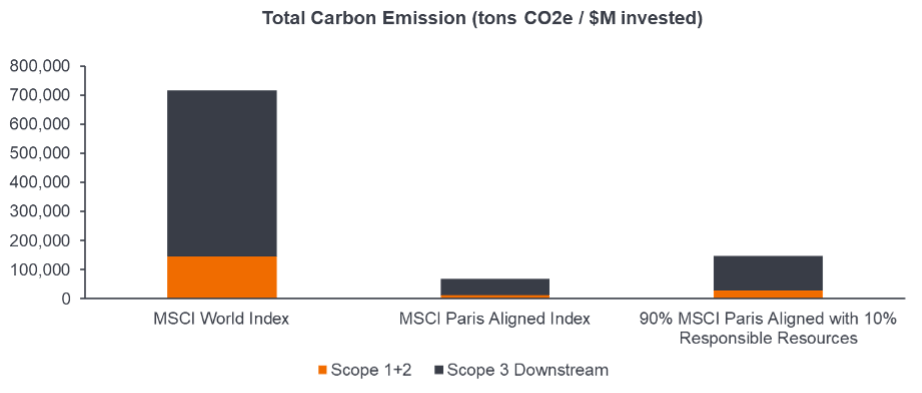

Source: Janus Henderson and MSCI, July 2023.

The fact remains that even sustainable resources companies will have higher carbon intensities than those of low-carbon indices. As Figure 2 shows investors can still achieve a significant reduction in the carbon profile of a portfolio by taking a blended approach, mixing investments in responsible resources with other low carbon equities.

Measures to acknowledge the role of company’s products and practices play in avoiding emissions (Scope 4) are starting to gain traction. A greater adoption of these metrics will help highlight the key contribution the resources sector play in physically decarbonising the economy.

In the meantime, investors should look beyond the carbon profile of their investments and ask whether their capital is ‘doing good’ by playing an active role in enabling a low- carbon future. Acceptance of a slightly higher carbon profile in some areas of the portfolio could be a better outcome for beneficiaries, than simply investing in a low-carbon portfolio that makes them feel good.

Important Information

The views presented are as of the date published. They are for information purposes only and should not be used or construed as investment, legal or tax advice or as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. Nothing in this material shall be deemed to be a direct or indirect provision of investment management services specific to any client requirements. Opinions and examples are meant as an illustration of broader themes, are not an indication of trading intent, are subject to change and may not reflect the views of others in the organization. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. No forecasts can be guaranteed and there is no guarantee that the information supplied is complete or timely, nor are there any warranties with regard to the results obtained from its use. Janus Henderson Investors is the source of data unless otherwise indicated, and has reasonable belief to rely on information and data sourced from third parties. Past performance does not predict future returns. Investing involves risk, including the possible loss of principal and fluctuation of value.

Not all products or services are available in all jurisdictions. This material or information contained in it may be restricted by law, may not be reproduced or referred to without express written permission or used in any jurisdiction or circumstance in which its use would be unlawful. Janus Henderson is not responsible for any unlawful distribution of this material to any third parties, in whole or in part. The contents of this material have not been approved or endorsed by any regulatory agency.

Janus Henderson Investors is the name under which investment products and services are provided by the entities identified in the following jurisdictions: Europe by Janus Henderson Investors International Limited (reg no. 3594615), Janus Henderson Investors UK Limited (reg. no. 906355), Janus Henderson Fund Management UK Limited (reg. no. 2678531), (each registered in England and Wales at 201 Bishopsgate, London EC2M 3AE and regulated by the Financial Conduct Authority) and Janus Henderson Investors Europe S.A. (reg no. B22848 at 2 Rue de Bitbourg, L-1273, Luxembourg and regulated by the Commission de Surveillance du Secteur Financier).

For use only by institutional, professional, qualified and sophisticated investors, qualified distributors, wholesale investors and wholesale clients as defined by the applicable jurisdiction. Not for public viewing or distribution. Marketing Communication.

Janus Henderson and Knowledge Shared are trademarks of Janus Henderson Group plc or one of its subsidiaries. © Janus Henderson Group plc.