Charlie Thomas

Has renewable investment already peaked?

Long-range forecasts suggest wind and solar will play an increasingly important role in the global energy mix. So why has the amount of money invested in renewable power fallen since 2015? Charlie Thomas considers this question and its implications for investors.

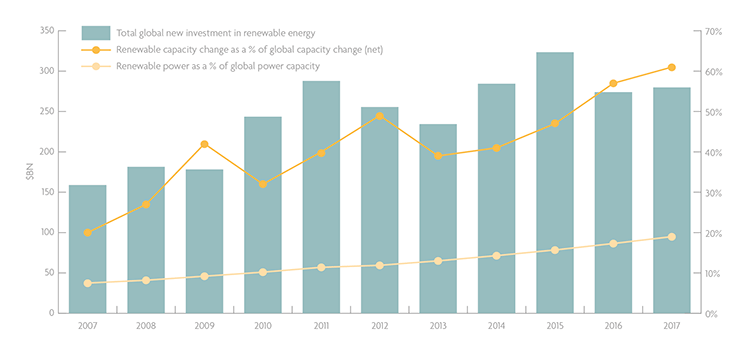

On many measures, renewable energy markets are flourishing. Data from the UN and Bloomberg New Energy Finance show that in 2007 renewable technologies accounted for 23% of new power capacity. Last year, this figure hit 61%, setting a new record of 157 gigawatts (GW) and far out-stripping the 70GW of net fossil fuel generating capacity added in 2017.[1]

Expectations for the longer term suggest the industry will be in rude health for some time yet. Forecasts suggest a 58% increase in global power demand between 2017 and 2040 and $10.2 trillion in investment in capacity to help meet this demand. Bloomberg analysts envisage a world in which wind and solar will account for some 48% of installed capacity and 34% of power generation. This implies a huge leap. To get there, investment in renewables will gobble up $7.4 trillion of the total spending on new capacity[2].

And yet, since the start of 2016 the amount of money invested in global renewable energy capacity has fallen.

Total global new investment in renewable energy vs. renewable power generation and capacity as a share of global power, 2007-2017, %

Source: UN Environment, Bloomberg New Energy Finance, http://fs-unep-centre.org/sites/default/files/publications/gtr2018v2.pdf

There is certainly some variation across regions. Investment peaked in Europe in 2011, flatlined in the US around the same time, and has hovered near its highs in China since 2016.[3] Nevertheless, the dampening of investment seems counterintuitive, especially given the healthy growth and project pipeline in the renewable energy sector.

In fact, this fall in investment is due to the key driver behind the boom in renewables: a dramatic drop in costs. Since the credit crisis, the pace at which wind and solar has become cost competitive has astounded many in the market, including us. Last September, two UK-based offshore wind projects won contracts at £57.50 per megawatt hour (MWh), placing these schemes among the cheapest electricity generated in Britain. In 2015, offshore wind power in the UK was priced at £117.14/MWh.

And these costs are expected to decline further in coming years. Estimates suggest the levelized or lifetime cost of electricity from solar could drop by a further 66% by 2040, while offshore wind power could see a 71% decline.[4] Thinking ahead, some energy analysts are moving beyond a scenario of constrained energy and rising prices, to one of potentially abundant, cheap and clean energy. The prospect would certainly have the potential to change the business case for investing in energy efficiency, a topic we will explore in more detail in a future article. But this is just one of several powerful investment implications that may lie ahead.

What does this mean for the investment opportunity?

Falling costs in the renewable energy sector are a sign of a rapidly maturing industry, able to construct projects at competitive prices and increasingly without subsidies. This in turn has attracted finance from large investor groups. Combined with increasing confidence in renewable technologies and long-term project viability, this is driving down the cost of capital and insurance costs, in turn stimulating further growth. For ambitious developers, this is a fertile environment for investment. The likes of Orsted see the market for offshore wind expanding well beyond Europe and becoming global ahead of even the most optimistic forecasts.

From a long-term investor’s perspective, the key consideration is whether the competitive tension amongst groups of project developers and renewable technology companies will remain healthy – driving down project costs and expanding the market for renewable energy, while sustaining attractive margins for equity investors. Margins may have come under pressure, but leaders are emerging, with seasoned management teams able to deliver on ambitious strategies.

For example, the wind and solar technology sector has already been in a process of rationalisation following the post-credit crunch collapse in project funding and prices. In the onshore wind sector, a relatively small number of key players with long project pipelines now dominate – names like Vestas, Siemens-Gamesa and GE – while the offshore sector is dominated by two competitors. China has its own industry.

Meanwhile, in a new development, open tenders for energy capacity mean that different types of renewable technologies are beginning to compete with each other and not solely against fossil fuels. While this makes sense from a cost point of view, competition between wind and solar has led to changes in business models. Vestas, for example, is repositioning itself as a provider of sustainable energy solutions rather than just wind energy technologies, a nod to the company seeing the opportunity for ’co-opetition’ (where businesses compete and cooperate to gain advantages) with other forms of renewables and other innovations.

This is not unique. Combinations of mature players and new innovators from across the energy and technology landscape are converging around solutions that are driving the next phase of growth.

Low-carbon ecosystems

For all the progress that renewable energy has made in recent years, passing notable landmarks along the way, we think that energy markets face a tipping point in the form of the current quest to break through the energy grid’s current 35%-40% renewable energy limit. This is rapidly becoming a constraint on further growth in renewables, as much of the world’s grid infrastructure simply isn’t ready for so much renewable power.

This is because a feature of the recent growth in renewable energy has been an increasing skew towards variable sources, principally wind and solar, which now make up almost four fifths of the new capacity.[5] There are days when renewable energy contributes 50% or more of the UK’s power needs. Germany hit a milestone in January this year when it sourced 100% of its electricity from renewables.[6] However, these are outliers rather than the norm. In general, current grid infrastructure was developed for predictable power from large power stations and struggles with more than 35%-40% regular contribution from variable renewable energy that is spread over larger areas.

The race is on to improve this rate while maintaining the grid’s stability. Leading the charge are countries that already have high amounts of variable renewables. Ireland recently set a new benchmark announcing that its grid can handle up to 65% variable renewable power at any time and is now focused on hitting the 75% mark.

Cases such as this show the combinations of solutions needed to achieve higher contributions from renewable sources: smart renewables and grid connections, and an emerging role for new forms of energy storage. Together, these are real-world low-carbon ecosystems addressing the challenge of what researchers at London’s Imperial College Energy Futures Lab recently summarised as an “interdependent, but not integrated, energy system”.[7]

We have some exposure to this ecosystem through holdings in established specialist companies such as Itron (smart meters and grid) and Prysmian (grid interconnectors). Some mainstream players are also venturing into this area. Offshore wind power company Orsted, which is also held in our portfolios, is currently involved in a project to provide a small 20-megawatt grid storage system to the UK’s National Grid, which will assist with grid stability.

Equally exciting are businesses developing and integrating new technologies. The combined energy storage and solar facility at the 50-megawatt Gannawarra Solar Farm in Victoria, Australia will enhance the local grid and provide solar power at night. While projects like this one are largely in a pilot phase, the success of this project could lead to further investment in combined renewable energy and storage projects, presenting new opportunities within the sustainable solutions themes that we may look to invest in. As a pivotal element of these low-carbon ecosystems, energy storage is a topic we’ll return to in more depth later this year.

Conclusion

Renewable energy costs are likely to continue on a downward path for some time yet. As a result, we expect to see investment in this area pause for longer or even decline further, even as installed capacity grows. Focusing on renewable energy investment in isolation, however, misses the bigger picture, in our view. With new solutions emerging in areas such as grid infrastructure and energy storage, capital is being invested across a wider low-carbon ecosystem. We therefore see real potential for overall investment rates to expand, supporting a new pool of investment opportunities for our portfolios.

Important Information: This document is intended for investment professionals and is not for the use or benefit of other persons, including retail investors. This document is for informational purposes only and is not investment advice. Market and exchange rate movements can cause the value of an investment to fall as well as rise, and you may get back less than originally invested. The views expressed are those of the Fund Manager at the time of writing, are not necessarily those of Jupiter as a whole and may be subject to change. This is particularly true during periods of rapidly changing market circumstances. Every effort is made to ensure the accuracy of the information but no assurance or warranties are given. Holding examples are for illustrative purposes only and are not a recommendation to buy or sell. Jupiter Asset Management Limited is authorised and regulated by the Financial Conduct Authority and its registered address is The Zig Zag Building, 70 Victoria Street, London, SW1E 6SQ, United Kingdom. No part of this commentary may be reproduced in any manner without the prior permission of Jupiter Asset Management Limited.

[1] Global trends in renewable energy investment 2018, UNEP & Bloomberg New Energy Finance. Figure excludes large hydropower.

[2] Source for all figures in this paragraph: Bloomberg New Energy Finance, New Energy Outlook, 15.6.2017, pg.3-4

[3] Source: Bloomberg New Energy Finance, Clean Energy Investment Trends, 1Q 2018, 11.04.2018

[4] Source for all figures in this paragraph: Bloomberg New Energy Finance, New Energy Outlook, 15.6.2017, pg.3-4

[5] Renewables and the Grid, A transformation in 3D, HSBC Global Research, 2017

[6] https://www.cleanenergywire.org/news/renewables-cover-about-100-german-power-use-first-time-ever

[7] https://www.imperial.ac.uk/news/185893/carbon-future-needs-integrated-energy-system/