Dave Whitehair, Director of Institutional Business (DC), Janus Henderson Investors

Co-Authors: James De Bunsen and Pete Webster – Portfolio Managers, Diversified Alternatives

The UK government wants DC schemes to play a much greater role in its’ “levelling up” agenda. For this to happen, it is our view that DC must join other institutional markets in investing more in alternative assets. Due to their alternative nature, these assets are often less liquid and may require a longer investment period before value is realised. Examples include private equity, private debt, venture capital, and infrastructure.

Closed-ended funds – another option for DC schemes

For DC schemes unwilling or unable to invest directly into alternative assets via private unlisted structures, the closed-ended fund market provides a viable option.

The popularity of closed-ended vehicles has been steadily rising, with alternative sectors driving that growth. A key reason behind this growth is that closed-ended funds, as permanent pools of capital, provide an ideal foundation for managers to invest in long-term opportunities, with the security that they will have no redemptions forcing them to sell down assets – a problem DC property funds have encountered several times in recent years.

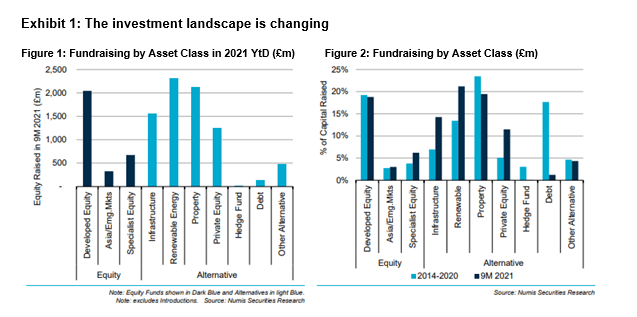

As Exhibit 1 shows, equity raisings for alternatives are significantly outpacing those in traditional asset classes. The UK-listed, alternative, closed-ended market is now £100bn by market capitalisation.

Source: Numis Securities Research, 1 January 2014 to 31 September 2021.

Note: For the left-hand chart, equity funds are shown in dark blue. Alternatives are shown in light blue. For the right-hand chart, the period 1 January 2014 to 31 December 2020 is shown in light blue; the period from 1 January 2021 to 30 September 2021 is shown in dark blue.

What closed-ended funds can offer DC investors:

- Liquid access to alternative assets: Fund structures that provide DC clients with daily liquidity have no minimum holding period or redemption notice.

- ‘Evergreen’ investment: In contrast to many private funds, closed-ended funds are effectively evergreen, with no end date for the portfolio, and they can support DC’s ongoing cashflows requirements.

- High governance standards: Closed-ended funds operate with independent boards that hold fund managers to account and provide timely and transparent reporting.

- Transparent performance returns: Closed-ended funds returns are straightforward, based on reported NAV and share price returns. Direct private funds, however, can adopt various return calculation methodologies that may change through time.

- Long-term opportunities in Impact Investing and ESG: Depending on their investment policies, closed-ended funds can provide bespoke access to the rapidly growing universe of impact and ESG-themed investment opportunities, such as social housing and renewable energy.

Closed-ended alternative asset classes available to DC investors

Private equity – provides access to early-stage, high-growth companies and buy-out opportunities. Private equity offers the opportunity to make higher returns than those of listed equivalents.

Specialist credit – less liquid, often physically-backed and/or senior loans/bonds that typically have floating rate coupons, providing protection from rising interest rates.

Infrastructure – Funding long-term infrastructure projects, either privately or in partnership with public bodies. Revenues are typically inflation-linked and non-cyclical in nature, given assets are critical to a functioning modern economy.

Renewable energy – Long-term funding of operational energy assets, predominately in the wind and solar sector, helping to tackle climate change. These deliver inflation-linked revenues and strong cash flow in the form of dividends.

Property – Liquid, low-cost alternatives (REITs) investing in physical real estate. In some cases, these are more aligned to infrastructure assets in nature than commercial property, such as social housing. Other specialist sectors such as student housing can offer higher yields.

In summary, we believe that as more DC investment decision makers turn their attentions to alternatives – and in particular private, illiquid assets – closed ended alternatives funds may represent a viable and useful tool for DC to gain exposure to this fast-growing asset class.

Important information:

The views presented are as of the date published. They are for information purposes only and should not be used or construed as investment, legal or tax advice or as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. Nothing in this material shall be deemed to be a direct or indirect provision of investment management services specific to any client requirements. Opinions and examples are meant as an illustration of broader themes, are not an indication of trading intent, are subject to change and may not reflect the views of others in the organization. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. No forecasts can be guaranteed and there is no guarantee that the information supplied is complete or timely, nor are there any warranties with regard to the results obtained from its use. Janus Henderson Investors is the source of data unless otherwise indicated, and has reasonable belief to rely on information and data sourced from third parties. Past performance does not predict future returns. Investing involves risk, including the possible loss of principal and fluctuation of value.

Not all products or services are available in all jurisdictions. This material or information contained in it may be restricted by law, may not be reproduced or referred to without express written permission or used in any jurisdiction or circumstance in which its use would be unlawful. Janus Henderson is not responsible for any unlawful distribution of this material to any third parties, in whole or in part. The contents of this material have not been approved or endorsed by any regulatory agency.

Janus Henderson Investors is the name under which investment products and services are provided by the entities identified in the following jurisdiction: Europe by Janus Capital International Limited (reg no. 3594615), Henderson Global Investors Limited (reg. no. 906355), Henderson Investment Funds Limited (reg. no. 2678531), Henderson Equity Partners Limited (reg. no.2606646), (each registered in England and Wales at 201 Bishopsgate, London EC2M 3AE and regulated by the Financial Conduct Authority) and Henderson Management S.A. (reg no. B22848 at 2 Rue de Bitbourg, L-1273, Luxembourg and regulated by the Commission de Surveillance du Secteur Financier); We may record telephone calls for our mutual protection, to improve customer service and for regulatory record keeping purposes.

For use only by institutional, professional, qualified and sophisticated investors, qualified distributors, wholesale investors and wholesale clients as defined by the applicable jurisdiction. Not for public viewing or distribution. Marketing Communication.

Janus Henderson, Janus, Henderson, Intech, Knowledge Shared and Knowledge Labs are trademarks of Janus Henderson Group plc or one of its subsidiaries. © Janus Henderson Group plc.