Bhavika Patel, Director, Global Business Development, & Blair Reid Partner, Senior PM – Multi Asset & Income, BlueBay Asset Management

Can multi-asset credit improve DC performance?

Multi-asset credit has played a growing role in defined benefit schemes for some years, although it still forms a very small part – if any – of most defined contribution (DC) allocations. We consider the merits of adding MAC to the mix for DC schemes by illustrating a range of portfolios in the 10-years leading to retirement.

Most DC lifestyles start with riskier assets, mainly equities, and gradually de-risk over time, often into diversified growth funds (DGFs) to target a desired retirement outcome. MAC does not typically feature, which raises the question: “Can exposure to MAC improve outcomes?”

What is MAC?

Multi-asset credit, or ‘MAC’, funds typically span the spectrum of credit asset classes and are characterised by their flexibility to allocate dynamically, rather than having fixed allocations. MAC funds come in many forms but in our examples we have included high yield bonds, bank loans, structured credit, cocos, convertible bonds and emerging market debt.

MAC versus DGF

DGFs also come in many shapes and sizes and are a popular inclusion in DC funds. They invest across a wide range of assets and the prime attraction is the expectation of equity-like returns with lower volatility. An example asset allocation might be:

| Equities | 50% |

| Investment grade bonds | 15% |

| Absolute return assets | 10% |

| Commodities | 10% |

| Property | 10% |

| Infrastructure | 2.5% |

| Private assets | 2.5% |

Modelling the performance of DGFs is not straightforward, given the variety of approaches. In the table below, we have selected a range of popular/large funds and averaged their performance.

Performance & volatility comparison over 10 years

| 10-year return | 10-year volatility | |

| DGF proxy | 4.9% | 5.4% |

| MAC | 5.3% | 4.4% |

Overall returns are similar, with MAC slightly ahead. In risk terms, MAC exhibits around 80% of the volatility of DGFs.

The merits of MAC

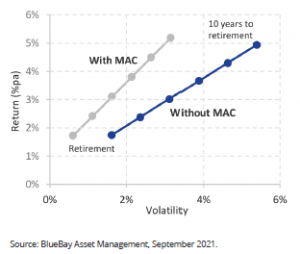

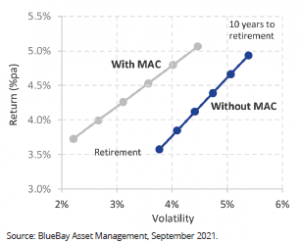

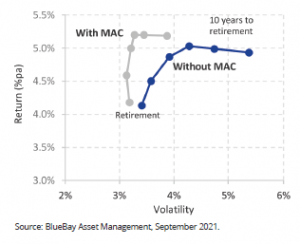

We introduced MAC allocations into three DC lifestyles to see how it impacted performance.

Profile 1: Cash lifestyle

This profile is a glidepath with a retirement mix of 70% cash and 30% DGFs. Substituting half the DGF exposure for MAC (15%) improves results by lowering risk without sacrificing returns.

Profile 2: Drawdown lifestyle

This profile is a glidepath with a retirement mix of 30% cash and 70% DGF. Substituting half the DGF exposure for MAC (35%) makes a notable difference in risk reduction. Returns are also higher with the addition of MAC and over the 10-year period, the pot size would be a GBP2,900 increase, based on a GBP100,000 starting portfolio.

Profile 3: Annuity lifestyle

Our final example considers a retirement exposure that includes 50% sterling Gilts and bonds at retirement, alongside 30% DGFs and 20% cash. Substituting half the DGF allocation with a 15% exposure to MAC again proves beneficial, making more difference in the early years when the exposure is higher. Based on a GBP100,000 starting pension pot, adding MAC improves the outcome by GBP2,300 over the 10-year period.

Conclusion

Across our three scenarios, adding MAC to the DC mix had a positive impact, with MAC contributing from both a risk and risk standpoint. One key attraction of MAC funds, in our view, is that the underlying assets are largely ‘contractual cashflows’, payable as long as a bond issuer does not default. This contrasts with equities, which can form a large component of DGFs, where equity dividends are not contractual.

For some time, MAC has been a popular choice for defined benefit funds, notably playing a role as pension funds have de-risked out of equities but do not want to sacrifice returns. In our view, MAC can play the same role for DC schemes, reducing volatility without necessarily reducing returns.

This document may be produced and issued by the following entities: in the European Economic Area (EEA), by BlueBay Funds Management Company S.A. (the ManCo), which is regulated by the Commission de Surveillance du Secteur Financier (CSSF). In Germany and Italy, the ManCo is operating under a branch passport pursuant to the Undertakings for Collective Investment in Transferable Securities Directive (2009/65/EC) and the Alternative Investment Fund Managers Directive (2011/61/EU). In the United Kingdom (UK) by BlueBay Asset Management LLP (BBAM LLP), which is authorised and regulated by the UK Financial Conduct Authority (FCA), registered with the US Securities and Exchange Commission (SEC) and is a member of the National Futures Association (NFA) as authorised by the US Commodity Futures Trading Commission (CFTC). In United States, by BlueBay Asset Management USA LLC which is registered with the SEC and the NFA. In Switzerland, by BlueBay Asset Management AG where the Representative and Paying Agent is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich, Switzerland. The place of performance is at the registered office of the Representative. The courts of the registered office of the Swiss representative shall have jurisdiction pertaining to claims in connection with the distribution of shares in Switzerland. The Prospectus, the Key Investor Information Documents (KIIDs), where applicable, the Articles of Incorporation and any other documents required, such as the Annual or Semi-Annual Reports, may be obtained free of charge from the Representative in Switzerland. In Japan, by BlueBay Asset Management International Limited which is registered with the Kanto Local Finance Bureau of Ministry of Finance, Japan. In Australia, BlueBay is exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of financial services as it is regulated by the FCA under the laws of the UK which differ from Australian laws. In Canada, BBAM LLP is not registered under securities laws and is relying on the international dealer exemption under applicable provincial securities legislation, which permits BBAM LLP to carry out certain specified dealer activities for those Canadian residents that qualify as “a Canadian permitted client”, as such term is defined under applicable securities legislation. The BlueBay group entities noted above are collectively referred to as “BlueBay” within this document. The registrations and memberships noted should not be interpreted as an endorsement or approval of BlueBay by the respective licensing or registering authorities. To the best of BlueBay’s knowledge and belief this document is true and accurate at the date hereof. BlueBay makes no express or implied warranties or representations with respect to the information contained in this document and hereby expressly disclaim all warranties of accuracy, completeness or fitness for a particular purpose. Opinions and estimates constitute our judgment and are subject to change without notice The document is intended only for “professional clients” and “eligible counterparties” (as defined by the Markets in Financial Instruments Directive (“MiFID”) ) or in the US by “accredited investors” (as defined in the Securities Act of 1933) or “qualified purchasers” (as defined in the Investment Company Act of 1940) as applicable and should not be relied upon by any other category of customer. No part of this document may be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, in whole or in part, for any purpose in any manner without the prior written permission of BlueBay. Copyright 2021 © BlueBay, is a wholly-owned subsidiary of RBC and BBAM LLP may be considered to be related and/or connected to RBC and its other affiliates. ® Registered trademark of RBC. RBC GAM is a trademark of RBC. BlueBay Funds Management Company S.A., registered office 4, Boulevard Royal L-2449 Luxembourg, company registered in Luxembourg number B88445. BlueBay Asset Management LLP, registered office 77 Grosvenor Street, London W1K 3JR, partnership registered in England and Wales number OC370085. The term partner refers to a member of the LLP or a BlueBay employee with equivalent standing. Details of members of the BlueBay Group and further important terms which this message is subject to can be obtained at www.bluebay.com. All rights reserved.