Jerry Song, Institutional Strategy & Analytics, J.P. Morgan Asset Management

Co-authors

Bob Cast, UK DC Client Advisor Alex Dryden, Investment Specialist

DC plans should consider adding multi-asset credit strategies to their default strategies

Executive Summary

An allocation to multi-asset credit can bring default portfolios more in line with the needs of today’s plan members, who are increasingly looking for options to stay invested up to and through retirement. Particularly in the mid phase of the glide path, plan members may be missing out on access to the attractive returns, diversification and downside protection that a multi-asset credit strategy can provide.

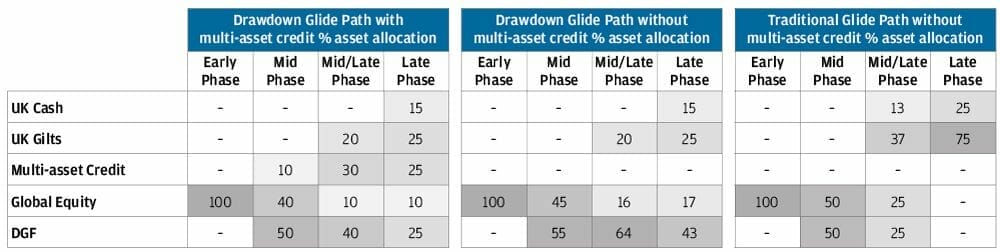

A MORE APPROPRIATE GLIDE PATH

A typical Defined Contribution (DC) default strategy begins to diversify away from equities in the mid phase of the glide path using diversified growth funds (DGFs), and by the late phase can be invested only in gilts and cash.

The blue line in the chart below shows the expected volatility and returns for a typical default allocation across the glide path, while the purple line shows the traditional allocations over time for DC plan members who choose a drawdown option at retirement.

The green line shows how risk-adjusted returns can potentially be improved by introducing a multi-asset credit allocation starting in the mid phase of the glidepath, which could be more appropriate for the needs of today’s DC plan members.

EXHIBIT 1: ADDING MULTI-ASSET CREDIT SHIFTS A MEMBER’S EFFICIENT FRONTIER

Source: J.P Morgan Asset Management, Long-Term Capital Market Assumptions as of 31 March 2020. Covariance estimates are based on historical monthly or quarterly returns from Q3 2006 to Q2 2019, depending on the reporting frequency of the underlying asset. For illustrative purposes only.

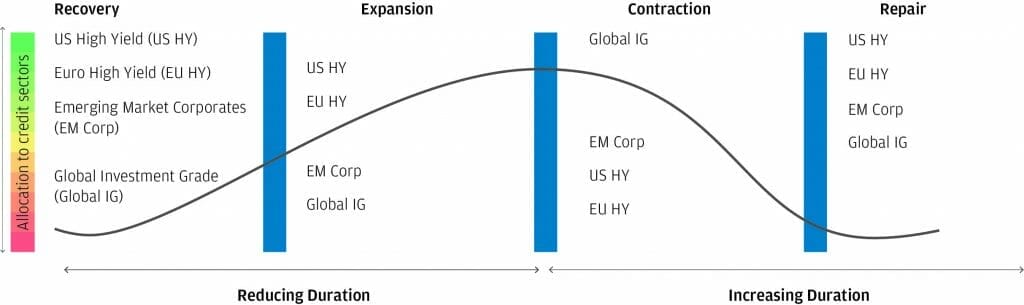

THREE WAYS THAT DC PLANS CAN BENEFIT FROM CREDIT EXPOSURE

Unconstrained credit makes DC fixed income allocations work harder

Multi-asset credit funds use flexible sector allocations (top-down) and rigorous security selection (bottom-up) to capture attractive returns with less volatility than the highest beta credit and fixed income sectors.

When considering the monetary policy backdrop, interest rates are likely to stay lower for even longer. In this environment, duration is unlikely to be a major contributor to overall returns for the foreseeable future. Instead, we see the credit risk premium and active sector and security selection playing an increasingly important role in driving performance.

The ability of flexible multi-asset credit funds to dynamically shift corporate credit allocations and interest rate sensitivity throughout the market cycle can help DC plans to improve the overall risk-adjusted return profile of their default strategy.

EXHIBIT 2: SECTOR AND DURATION POSITIONING IS ACTIVELY MANAGED THROUGH THE MARKET CYCLE

Source: J.P Morgan Asset Management. For illustrative purposes only.

Dynamic credit can capitalise on more alpha opportunities while limiting risk

An unconstrained approach gives managers the freedom to express their views. If they do not like a sector or a name, they don’t own it. This flexibility enables managers to react quickly to risk events and take advantage of opportunities across the full corporate credit universe as they arise.

Although managers have the freedom to invest in their favoured segments of the market, all of this can be conducted within a robust risk management framework that ensures risk is managed within pre-defined limits.

Diversified credit exposure can produce a smoother investment journey for DC members

Diversification plays a key role in producing attractive risk adjusted returns. This can be achieved by accessing a truly global opportunity set, including both developed and emerging markets, allocating across different asset classes and taking exposure to a wide range of companies and sectors with varying business models. The below chart shows the protection that this diversified approach can have in protecting on the downside by limiting the overall drawdown of the investment journey.

EXHIBIT 3: MULTI-ASSET CREDIT HAS DEMONSTRATED A LOWER DRAWDOWN PROFILE THAN OTHER ASSET CLASSES

Source: J.P. Morgan Asset Management, Bloomberg. All rights reserved. Data as of 31 June 2020. Multi-Asset Credit = J.P Morgan Multi-Sector Fund I (acc) USD Hedged. U.S High Yield = Bloomberg Barclays US Corporate High Yield Total Return Index, EM USD = Bloomberg Barclays EM USD Aggregate: Corporate, Global IG = Bloomberg Barclays Global Aggregate Corporate Total Return Index Hedged USD. US equities = S&P 500.

FOR PROFESSIONAL CLIENTS/ QUALIFIED INVESTORS ONLY – NOT FOR RETAIL DISTRIBUTION: This is a marketing communication and as such the views contained herein are not to be taken as advice or a recommendation to buy or sell any investment or interest thereto. Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are, unless otherwise stated, J.P. Morgan Asset Management’s own at the date of this document. They are considered to be reliable at the time of writing, may not necessarily be all inclusive and are not guaranteed as to accuracy. They may be subject to change without reference or notification to you. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and investors may not get back the full amount invested. Past performance and yield are not a reliable indicator of current and future results. There is no guarantee that any forecast made will come to pass. J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our EMEA Privacy Policy www.jpmorgan.com/emea-privacy-policy. This communication is issued in Europe (excluding UK) by JPMorgan Asset Management (Europe) S.à r.l., 6 route de Trèves, L-2633 Senningerberg, Grand Duchy of Luxembourg, R.C.S. Luxembourg B27900, corporate capital EUR 10.000.000. This communication is issued in the UK by JPMorgan Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority. Registered in England No. 01161446. Registered address: 25 Bank Street, Canary Wharf, London E14 5JP. Copyright 2020 JPMorgan Chase & Co. All rights reserved.

0903c02a829ee611